Silicon Valley Bank and the Implications for National Currency

I, many friends, our entire industry, and perhaps you are reeling from the rapid collapse of three US banks serving the broader tech & crypto sectors: Silicon Valley Bank, Silvergate and Signature.

Much fantastic analysis has been done on the causes and impacts of the bank failures themselves, including some of my favorites by Luca, Lex and Ayo.

Rather than replay the events or rework the analysis, after a week of reflection, I find myself thinking about what comes next.

While any contagion from the three bank collapses appears to have been averted through aggressive actions by the US government in the form of a full deposit backstop over and above FDIC limits, risk in the banking system is clearly growing.

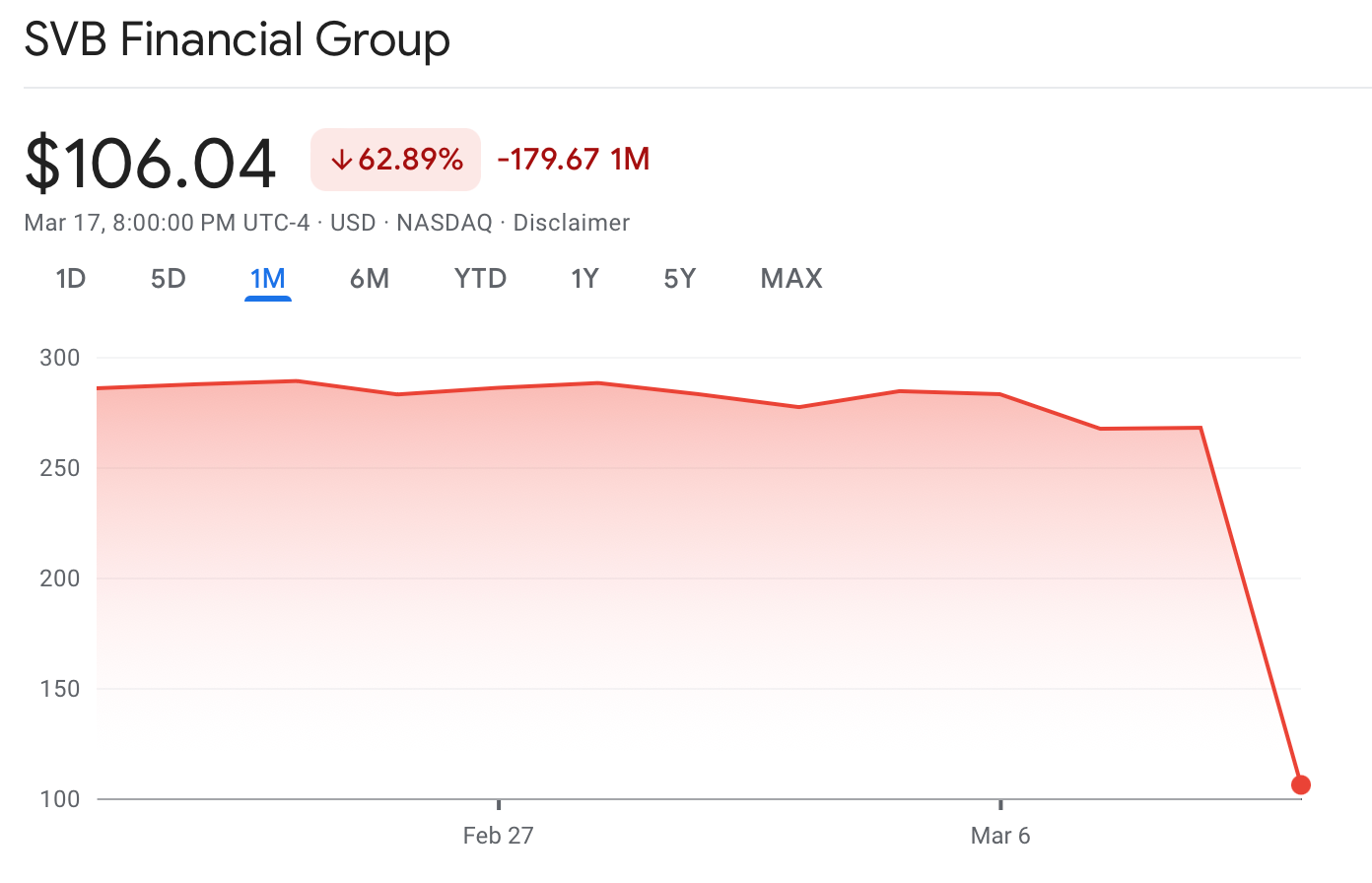

The lightning bank run Silicon Valley Bank (SVB) experienced was shocking in its speed and scale, driven by internet-wide social coordination via Twitter and the ease and immediacy of large volume deposit withdrawals. SVB was the first time we've seen these tools fuel a bank run, but there's no reason to believe it will be the last. Post SVB, no non-Global Systemically Important bank feels safe.

SVB's startup and VC heavy depositor base was intimately connected with global institutional capital and consumers, SMBs and corporates in the US and abroad, meaning the impact of deposit losses would have been far-reaching. As a simple example, USDC, one of the internet's reserve currencies, traded down 10% on news that $3b of its collateral was on deposit with SVB.

In similar fashion, the recent growth of the banking-as-a-service model has extended the deposit reach of dozens of community and regional banks beyond their local geographies, potentially pushing fallout from such a bank failure nationwide through interconnected dependencies.

Today, you could build a system in your bedroom to automate cash management across banks, incorporating triggers like social media sentiment analysis, real-time share price performance and regulatory filings instantly parsed and interpreted by AI. Combine it with immediate access to withdrawals through online banking & mobile apps and the impending availability of FedNow, roll it out at scale, and it becomes difficult to imagine how a bank could survive a serious stress event. This reality has fundamental implications for our current model of fractional reserve banking, a standard conceived centuries ago in a different world.

In short, the potential for bank runs appears to be increasing while the impact of the failure of certain non-GSIBs simultaneously grows.

What can we do?

Technology created this situation and also presents numerous potential solutions, in conjunction with thoughtful, proactive, real-time regulation.

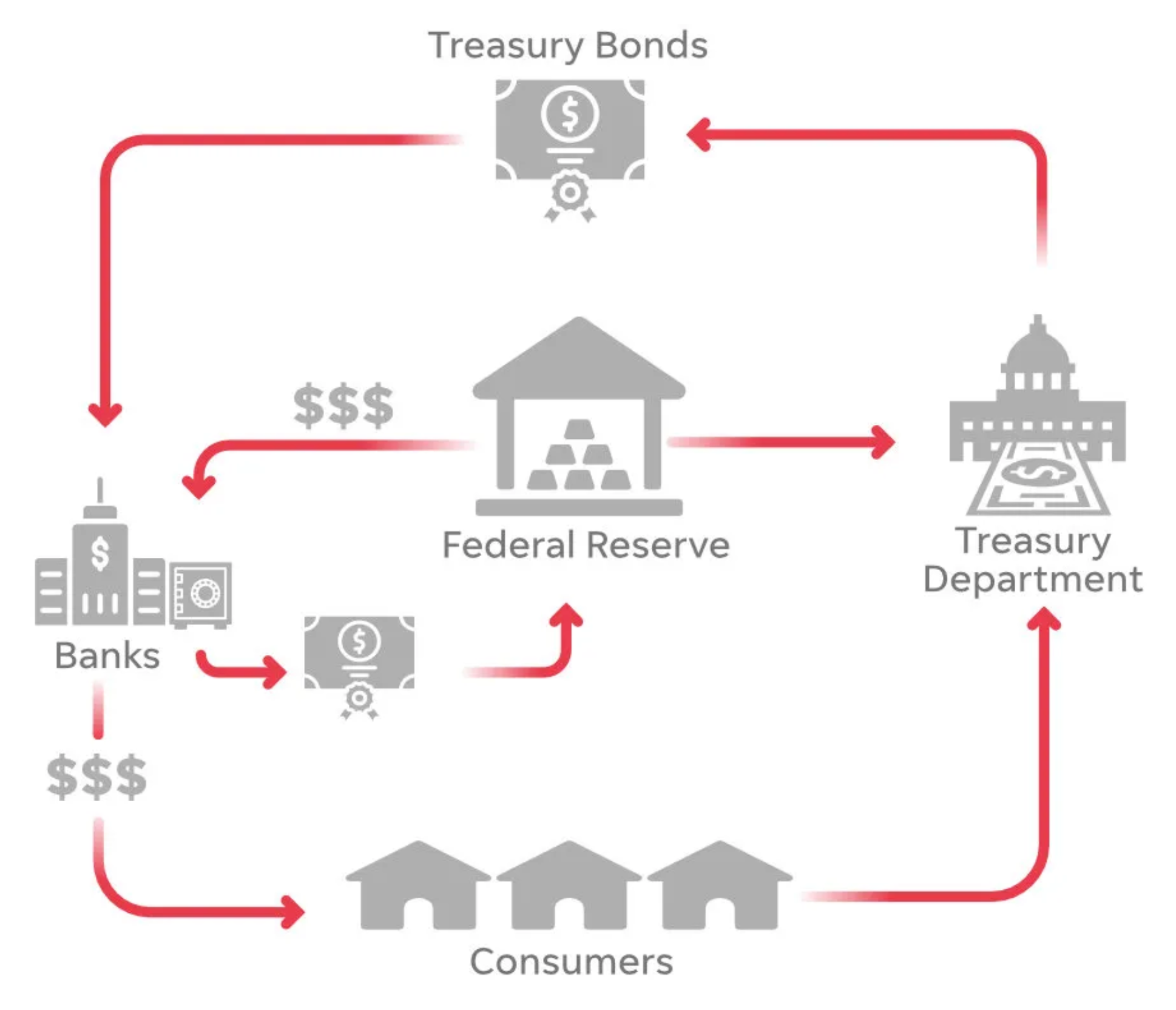

Banks intermediate many interactions between nation states, private individuals and companies and create value, risk and complexity in the process. For example, banks underwrite loans to fund economic activity, aggregate lending to the government, theoretically safeguard cash balances, facilitate payments and spending, and much more.

This suite of interrelated functions is bundled into the modern day bank. Is that the optimal configuration?

There's an argument that currency access need not be intermediated by banks, while related services very much remain valuable for banks to provide. A full government backstop of deposits, as seen in the wake of the SVB collapse, effectively overrides the fractional reserve model, with banks + governments fully collateralizing deposits or at least guaranteeing liquidity to all depositors.

This regulatory approach, effective as it was in limiting contagion over the past week, creates adverse incentives and moral hazard in banking.

So what other options are there?

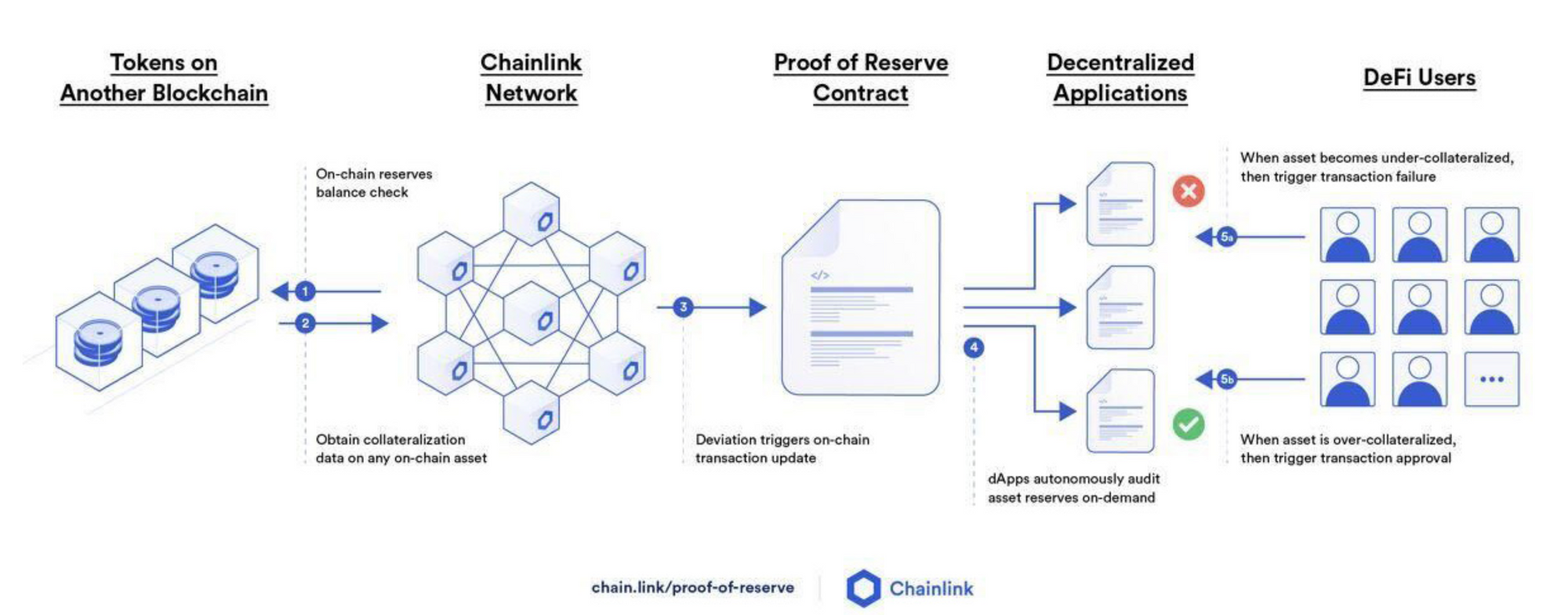

The crypto space is addressing the issue of centralized intermediary stability (the risk of the exchange failing and losing your money) with a blockchain-based approach, namely Proof of Reserves. In such a model, intermediaries provide transparency by publicly verifying the details of their assets and liabilities, even though not required to do so by law.

In a sector of such national importance as banking, it is reasonable to insist on extreme levels of verifiable, machine readable transparency about assets and liabilities, and by extension capital and liquidity.

However, important as increased transparency is, it doesn't prevent bank runs.

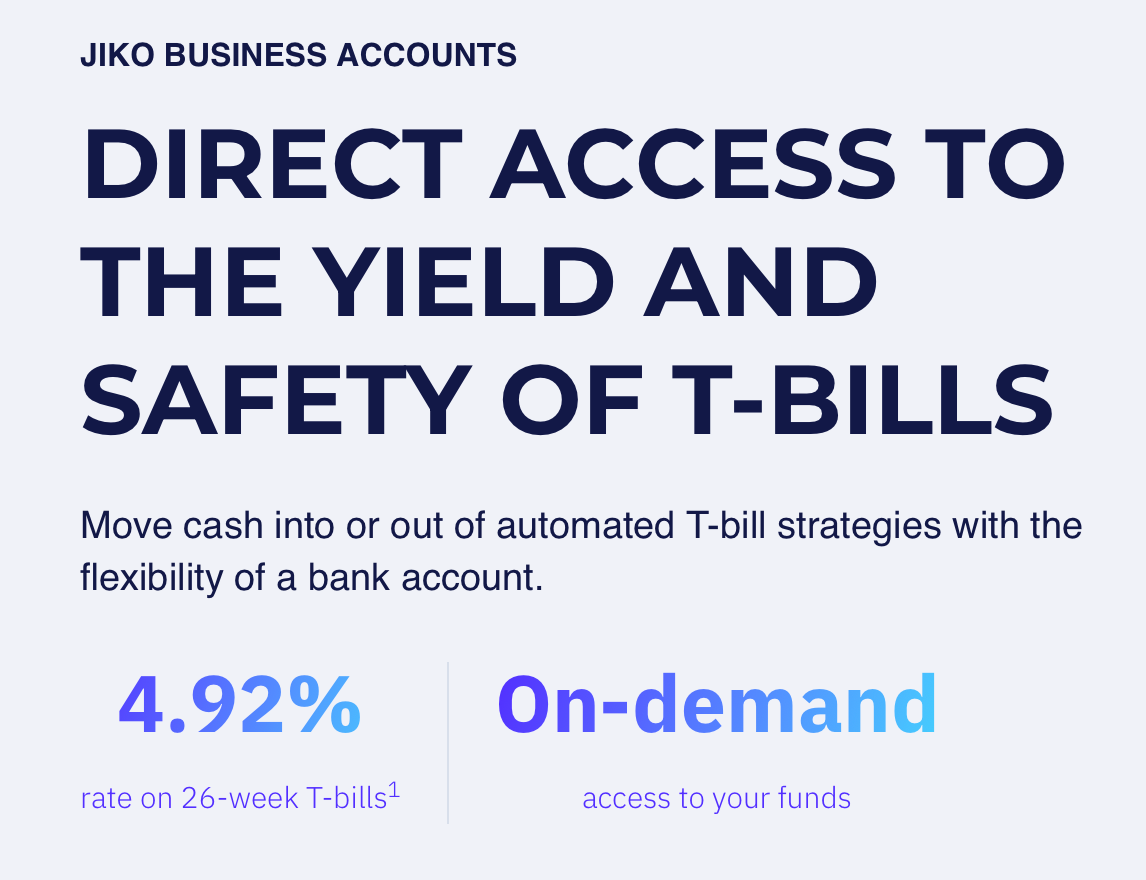

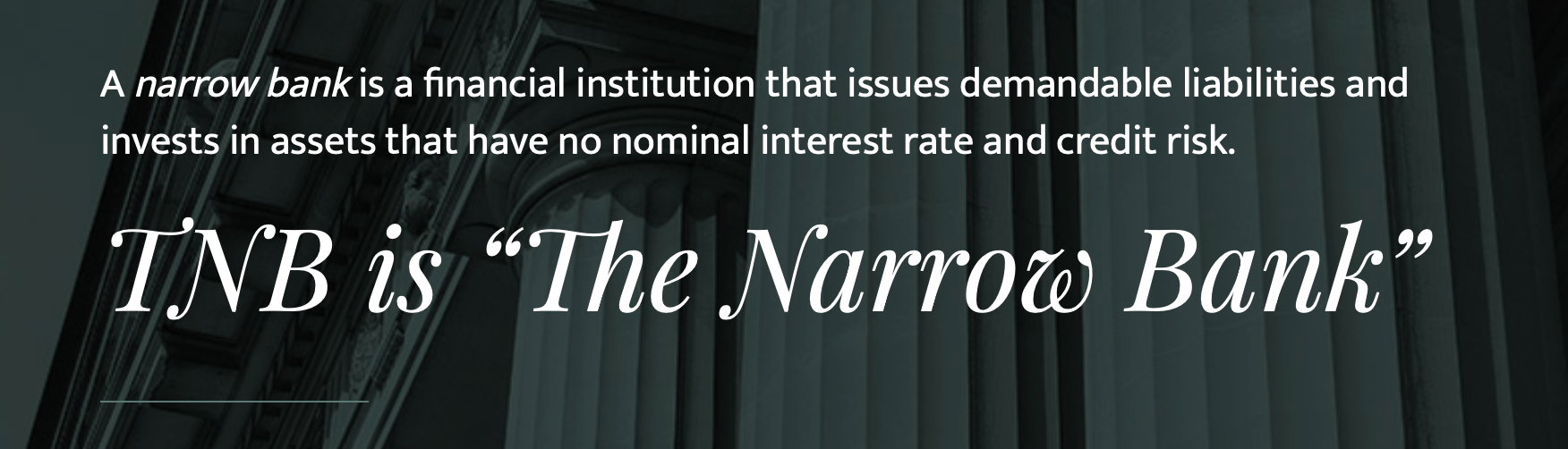

New approaches to deposits and cash management are being built with core assumptions that depart from fractional reserve thinking. Jiko is creating a transaction account layer for banking based on direct ownership of US Treasuries, effectively taking steps toward a privately built USD CBDC proxy. TNB is trying to provide institutional depositors with direct access to Central Bank accounts, eschewing both commercial bank intermediation and the fractional reserve model (and reportedly meeting regulatory resistance to its efforts).

Interestingly, two of the beneficiaries of the SVB failure and associated contagion fears were Bitcoin and Ether, which pumped while the banking sector shuddered. In part, their price performance may have been driven by expectations of a halt/reversal of interest rate actions, benefitting risk-on assets, but a rush to self-custodied stores of value undoubtedly contributed to the gains. Ironically, it was these two assets, with no underlying reserves, collateral or government guarantees, that performed best during peak banking sector instability.

Given the mounting risks associated with the current bank deposit model, it is increasingly difficult to imagine a future state in which direct retail and business access to liquid, exchangeable government liabilities does not become commonplace. For such a model to be most robust, it should also incorporate the transparency and audibility being pioneered by blockchain/web3.

The development of higher integrity currency, with new native properties like permissioning and yield that modern technology can support, may be the innovation that connects fiat and web3 to deliver safer, transparent and more fundamentally sound financial systems and economies.